January 7, 2026

“Be fearful when others are greedy and greedy when others are fearful.”

As you may have heard, December 31, 2025, not only marked the end of the calendar year but also the end of the career for possibly the greatest investor of all time as Warren Buffett retired from running Berkshire Hathaway (at the spry age of 95). While there is no shortage of quotes to choose from over his 70+ year career, the saying above is probably one of the most well-known and perhaps appropriate for where we are in time. After all, the “Buffett Indicator,” which comprises the ratio of the stock market value to the size of the economy (GDP), stands at an all-time high (see chart below). Buffett also exits Berkshire leaving a cash hoard of over $380 billion from selling stocks and businesses over the past several years. He appears to be literally taking his own advice expressed above. While Berkshire’s stock did underperform the S&P this year (+10.9% vs. +17.9%), over time the comparison is not even close.

Over the past 35 years, Berkshire’s A-shares are up over 11,200% vs. the S&P 500’s 4,000% return. As the disclosure goes, past performance is no guarantee of future results and Buffett’s successor Greg Abel certainly has big shoes to fill (ask the head coach of Alabama Kalen DeBoer how easy that is). Still, it seems to me we should not ignore the Oracle of Omaha’s parting message. As we move on to other subjects below, I’ll throw one more Buffett-ism at you – “In the business world, the rearview mirror is always clearer than the windshield.” Enjoy retirement Warren, you’ve quite literally earned it.

Venezuela

As we begin the year, the windshield is fogging up quickly. We will start with the most recent event, that being the extraction and arrest of Venezuela’s president, Nicolas Maduro, by US armed forces. I must admit, while I remember learning about the Monroe Doctrine and the Roosevelt Corollary in history class, I had to refresh my memory as these were being thrown around in the news regarding this situation. To terribly oversimplify it, this policy, declared by President James Monroe in 1823 and later expanded by President Theodore Roosevelt in 1905, stated that the US “controlled” the Western Hemisphere and, at that time, Europe should mind their own business. Roosevelt went on to say that the US should be allowed to intervene in Latin American countries to stabilize them. That is digging deep, back over 200 years, for the “justification” of the move.

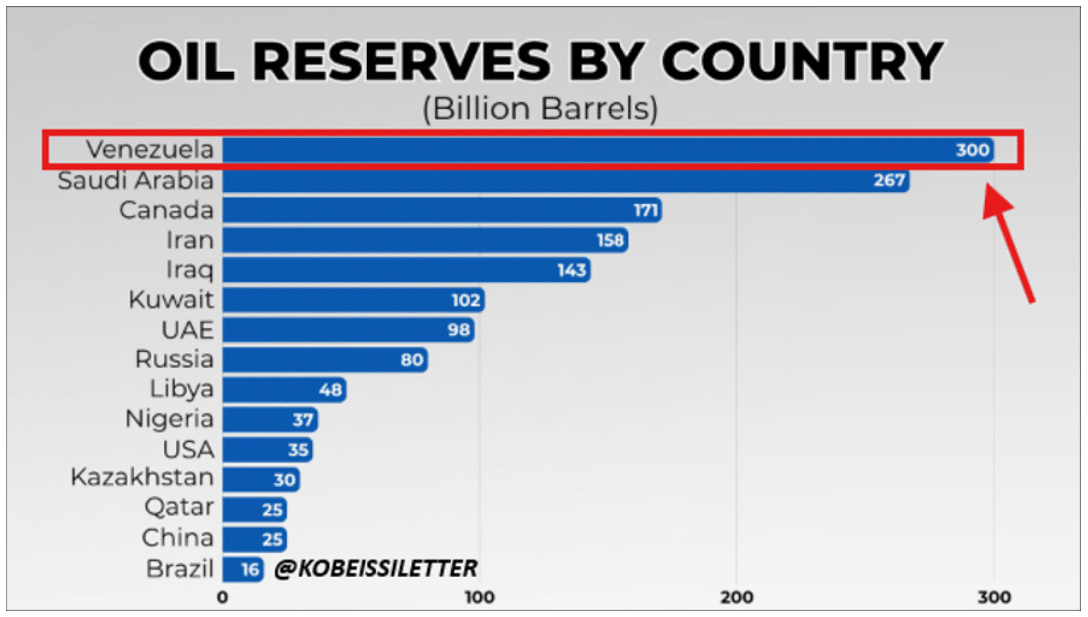

The chart and picture may be a more realistic explanation. The chart left shows that Venezuela has the largest oil reserves of any country in the world. This crude is also “heavy crude” which US refiners are built to process. While Venezuela’s current crude production is down significantly from its peak of over 3 million barrels per day (bpd) due to a lack of investment, it still produces around 1 million bpd, and the biggest importer of Venezuelan crude is China.

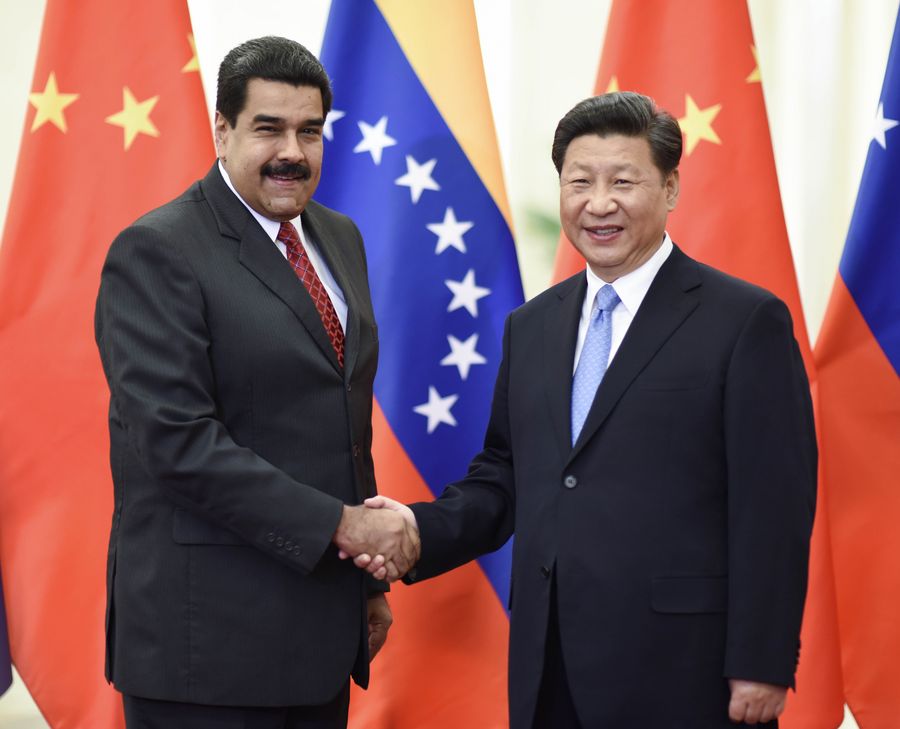

Which brings us to the picture of Maduro and Chinese President Xi shaking hands. This appears to be not just a resource play for the US but also a move to keep those same resources from China or at least have quasi-control over them. The market reaction to these events is interesting as I sit at my desk on the morning of January 5th. There is a risk-on tone to asset prices, but I’m not sure the world became a less risky place as a result of what happened. Seemingly another brick in the wall of worry for the market to climb, perhaps not dissimilar from the US bombing of Iran’s nuclear facilities in June. That is probably more than enough time dedicated to a geopolitical discussion, but I have a feeling we will be talking about this one for a while.

Government Affairs

Staying on the topic of government affairs, there are a few items to watch in January. First, we have the potential for another government shutdown at the end of January. Congress must come to a budget deal or pass a continuing resolution by that time to avoid closing the government yet again. Both sides have signaled their desire to avoid this outcome, and odds in the betting markets are below 25% that a shutdown will occur. Still, the events over the weekend could complicate negotiations. Stay tuned. In addition, we could get a ruling from the Supreme Court in late January or early February on the legality of the tariffs implemented under the International Emergency Economic Powers Act (IEEPA). President Trump utilized this authority to enact many of his tariffs in 2025. Should the Supreme Court rule against him (and betting markets are saying there is a 78% chance they will), there could be some temporary confusion in the market on the path forward. There are other powers that can be used to quickly reinstate tariffs should this outcome occur, but there could be a lingering question as to whether the US must refund tariffs already collected. If so, we could see upward pressure on interest rates.

Financial Markets

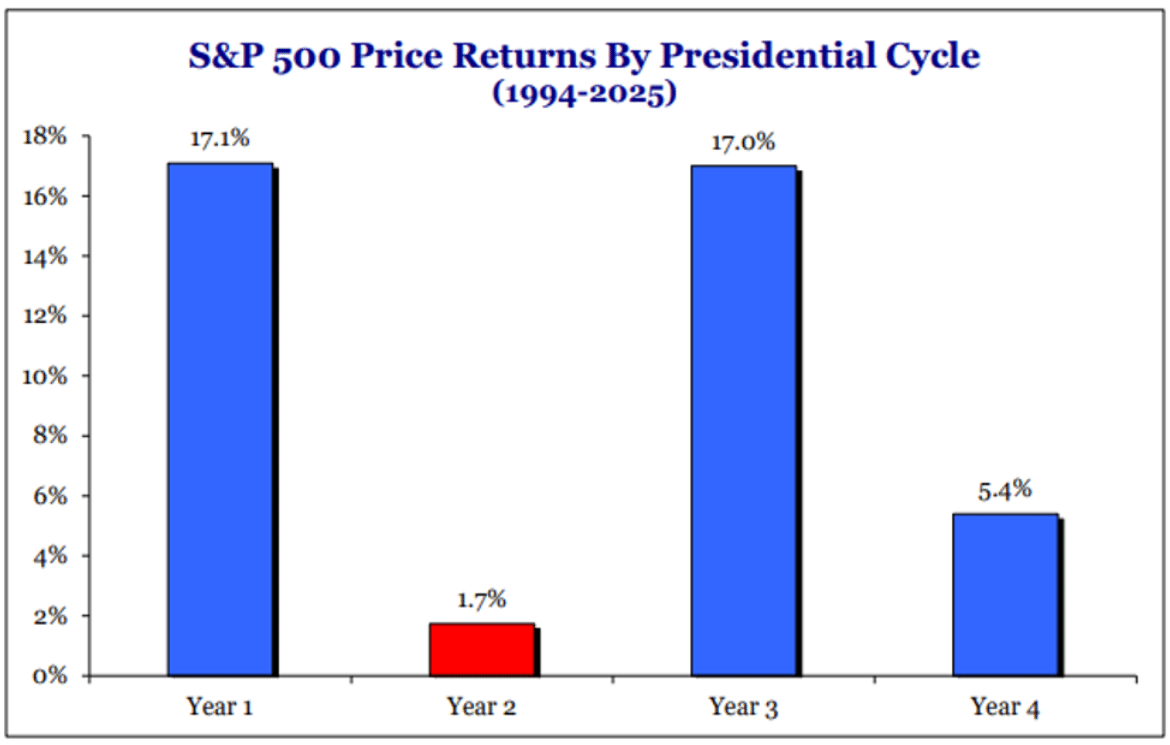

Moving to financial markets, we provide a detailed breakdown in our Market Commentary regarding equity and fixed income investment performance. Long story short here: It was a good year for nearly all asset classes. For equities specifically, it was the third consecutive 15%+ return year for the S&P 500 Index. This is just the fourth occurrence since 1926 that markets have seen such a winning streak. Prior episodes in the early 1940’s, early 50’s and mid 90’s, all saw a fourth year of 15%+ returns. The exception was recently in 2022, where the S&P was down -18% following a three-year run from 2019-2021. A potential headwind for 2026 is the historical performance of markets during a mid-term election year. The chart from Strategas on the following page shows the past thirty years of data on returns by year of the Presidential Cycle. Year 2 is by far the worst of those. Certainly, no guarantee of a good or bad outcome, but some historical context for consideration. The annual pattern of the year 2 return is also worth noting with weakness typically concentrated in the second and third quarters of the year before turning higher the closer you get to the election in November. Should this pattern play out in 2026, we will look to take Buffett’s advice and “look at market fluctuations as your friend rather than your enemy.” The good news is that in the 12 months following a mid-term election, we have not seen a negative return in any year going back to 1938.

The Federal Reserve

The final topic I will touch on is the Federal Reserve. We should get an announcement of a new Fed Chairman early this year. Jay Powell has been in the seat for roughly eight years, appointed by President Trump during his first term. His term as Chairman ends in May. The battle for the new Chairman is between Kevin Hassett, current Director of the National Economic Council, and Kevin Warsh, a former Fed Governor from 2006-2011. The betting markets have Hassett’s odds at 42% and Warsh’s at 37%.

Why does this matter? There is a line of thinking that the appointment of Hassett could push long-term interest rates higher if market participants assign low credibility to his independence as the Fed Chairman and his willingness to hold the line on inflation. We actually have some evidence of this dynamic in October and November of last year, as his odds of being appointed rose to a high of 85%, the 10-year Treasury moved 30 basis points higher.

In addition to this external impression of Hassett, within the Fed itself, I believe he would have a hard time gaining consensus, given his lack of institutional experience, perhaps prompting Powell to remain as a Fed Governor until his term in that role expires in 2028 (just his role as Chairman expires in May 2026). On the other hand, Warsh has the unique combination of having institutional knowledge, particularly during the Financial Crisis in 2007-2009, but has been removed from the Fed for long enough to bring a fresh perspective to the job.

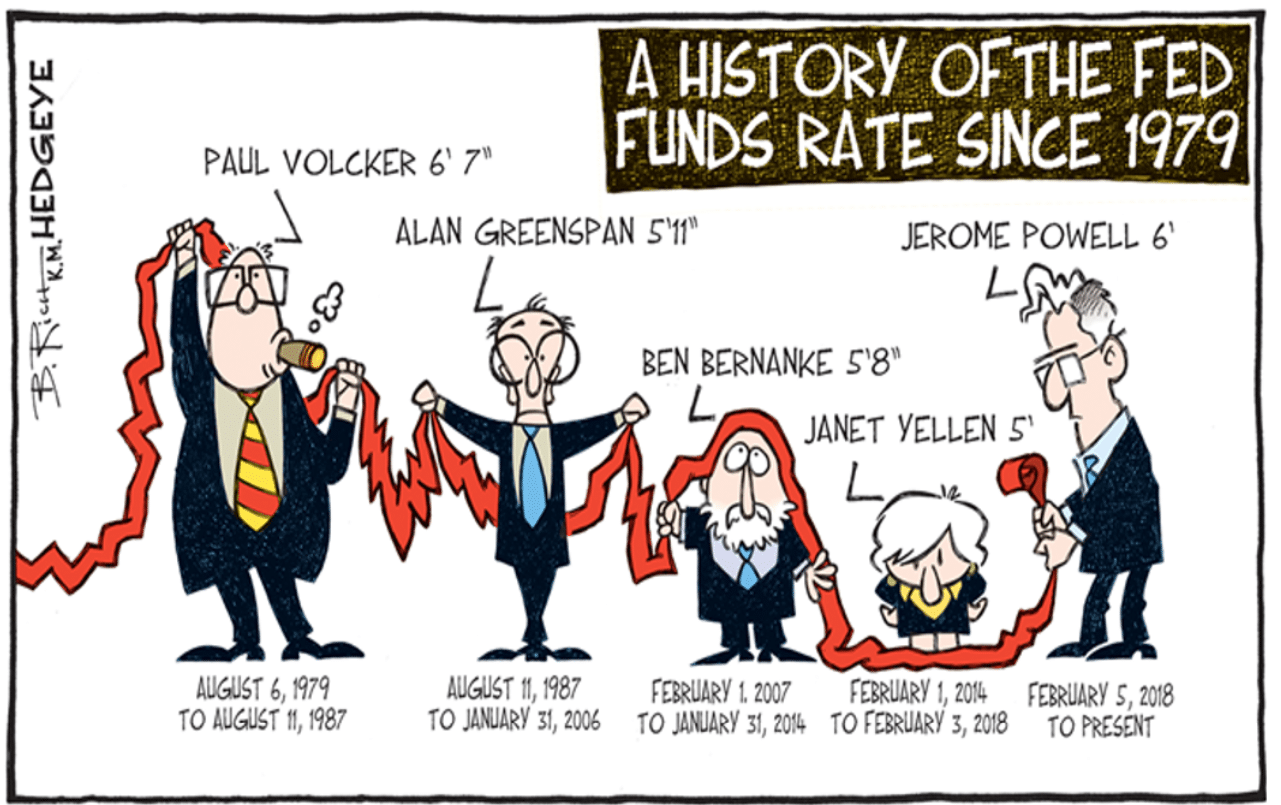

Regardless of who gets the job, history would suggest that they will get a test of their skills early in their tenure. Given past experience, Warsh may be better equipped to pass that test. As far as the direction of rates based on the height of the Fed Chairman (see cartoon), ChatGPT tells me that Warsh is taller than Hassett but unclear vs. Powell.

Firm News

In firm news, we are excited to announce the addition of a new Associate Advisor in Greenwood, Brandon Williams. Brandon is a graduate of Presbyterian College (Go Blue Hose) and joins us from a recent role at an RIA in Lexington, SC. He will be working with John Cooper in Greenwood. Welcome aboard. As always, thank you for your continued confidence in and support of Greenwood Capital. If you enjoy working with our team, I would like to invite you to consider writing a Google review for our firm. In this new world of AI generation and digital content, a few words from real people can make all the difference. Please do not hesitate to call or email with any questions.

On behalf of all the employees at Greenwood Capital,

Sincerely,

Walter B. Todd, III

President/Chief Investment Officer

The information contained within has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy. The opinions expressed are subject to change from time to time and do not constitute a recommendation to purchase or sell any security nor to engage in any particular investment strategy. Investment Advisory Services are offered through Greenwood Capital Associates, LLC, an SEC-registered investment advisor.